Why Three Generations Are Failing at Retirement Planning

It didn't arrive as a single moment. It was more like a slow discomfort that kept returning, until it became impossible to ignore.

Early in my career, the work felt clean. Build a portfolio, project a return, show a retirement number. Clients liked the clarity. The industry liked the simplicity. But somewhere in my late 30s, patterns started to repeat in ways the models couldn't explain.

Two clients could retire with the same "number" and live completely different realities. One slept well. The other quietly unraveled within a few years.

When Arrival Replaced Survival

The first real crack came after sitting with a client who had technically "won." Strong portfolio, disciplined saver, retired on schedule. But three years in, a market drawdown forced him to cut spending at the exact moment his identity was already in transition.

The spreadsheets had assumed average returns. His life experienced sequence. That gap wasn't small. It was structural.

That was when it started to feel like the industry was optimizing for arrival, not survival. We were trained to answer, "How much do you need to retire?" But almost no one was seriously asking, "What needs to keep working when things don't go to plan?"

The Vanguard 2025 report confirms what I've been seeing across the table for years. Only 40% of Baby Boomers are on track for retirement readiness. Gen X sits at 41%. Millennials at 42%. For median-income Boomers earning $56,000 annually, retirement savings are projected to replace just 56% of pre-retirement income, leaving an annual shortfall of $9,000.

But those numbers don't tell you why the gap exists. They don't explain why three generations, with access to more financial tools than any generation before them, are still struggling with the same fundamental problem.

The System Shifted Risk Without Redesigning Plans

Here's what actually happened. A generation ago, income in retirement had more built-in stability. Pensions were more common. Career paths were more linear. Housing costs were lower relative to income.

Today, much of that stability has been replaced by individual responsibility. People are expected to invest their way to certainty, but markets were never designed to provide predictable income on demand.

The data shows this clearly. Workers with access to defined contribution plans are nearly twice as likely to be on track for retirement (54%) compared with those without access (28%). Only 35% of workers had access to DC plans in 1989, rising to 52% by 2022.

But here's the uncomfortable part. Baby Boomers entered the workforce before the widespread adoption of modern defined contribution plan features that became common only after the Pension Protection Act of 2006. They missed the structural shift. Not because they were undisciplined, but because the system changed underneath them.

In Singapore, the same pattern shows up differently. The CPF system represents one of the most well-designed retirement frameworks in Asia. Singapore ranked 5th worldwide in the 2025 Mercer CFA Institute Global Pension Index with an 'A' grade for the first time, positioning it as the top retirement system in Asia.

But even here, the transition from employer-managed certainty to individual responsibility happened faster than meaningful financial education could reach older workers. The 2025 CPF reforms raised contribution rates for workers aged 55-65 by 1.5 percentage points, with the monthly salary ceiling increasing from $6,800 to $7,400. The payout eligibility age increased from 65 to 66 starting in 2025 for those born in 1960.

The system is adapting. But many people are still operating with frameworks built for a world that no longer exists.

What Actually Breaks When Accumulation Meets Decumulation

Over time, a few uncomfortable truths became clearer. Returns were treated as the main lever, but behavior was doing most of the damage. Clients didn't fail because markets underperformed by 1 or 2 percent. They failed because they panicked, overspent early, or couldn't adjust when life deviated from plan.

Yet most portfolios were still built as if behavior would remain perfectly rational for 30 years.

Income was treated as a byproduct of assets, instead of something to be engineered deliberately. I saw retirees with sizable portfolios but no clear income floor. Everything depended on withdrawals. That works beautifully on paper. It feels very different when every market dip becomes a personal pay cut.

The research on sequence of returns risk confirms this. Wade Pfau estimates that approximately 77% of a portfolio's final retirement outcome can be explained by the returns of just the first 10 years of retirement. When markets fall early in retirement, investors are forced to sell more shares to fund the same withdrawal at exactly the wrong time. Those shares are gone forever and can't participate in the eventual recovery.

Two retirees with identical portfolios and average returns can experience nearly $500,000 difference in ending values solely based on when losses occur. Negative returns during the first five years account for 70% of retirement plan failures.

But the industry still presents retirement as if it's just accumulation in reverse.

The Difference Between Having Enough and Feeling Secure

What looked like the same outcome on paper was built on very different internal structures. The client who slept well didn't actually think in terms of a "number." Somewhere along the way, his plan had shifted from accumulation to continuity.

About five to seven years before retirement, he started carving out a base layer of income that didn't depend on markets. Part of it came from CPF LIFE, part from a simple bond ladder, and a small rental stream that was never meant to maximize yield, just stability.

So when markets moved, his lifestyle didn't have to. His essential expenses were already spoken for. What sat in equities became psychologically reclassified. It wasn't "my retirement money" anymore. It was "long-term capital."

That distinction sounds subtle, but it changes behavior completely.

The client who unraveled had just as much, sometimes more. But everything was tied to a single pool. Investments were meant to grow, and then be drawn down to fund life. On a spreadsheet, the probability of success looked high. But in real life, every withdrawal became a decision. Every market dip felt like a threat to income, not just to wealth.

When markets fell 15 percent, the first client adjusted nothing. Income kept flowing. The second client started recalculating. "Should I reduce withdrawals?" "Is this the start of something worse?" That constant need to decide slowly eroded confidence.

Converting Wealth Into Certainty

That language didn't come from training. In fact, I had to unlearn quite a bit before it started to make sense. Early in my career, "good advice" was tightly linked to efficiency. Keep money compounding. Avoid locking it up. Maximize optionality.

But over time, the lived experience of clients kept pushing back against that idea.

I started noticing that the clients who felt the most at ease in retirement weren't the ones with the highest returns or the largest portfolios. They were the ones who had deliberately given up a portion of upside in exchange for predictability.

Then a pattern became clear. Uncertainty isn't evenly distributed across a plan. It concentrates around cash flow. You can tolerate your portfolio fluctuating. What most people struggle to tolerate is their income fluctuating.

In Singapore, that often showed up in how clients engaged with CPF LIFE. Early on, many treated it as something to minimize or optimize around. Later, I began to see it differently. Not as a return-generating tool, but as a psychological anchor. A base layer that removed the need to make decisions under stress.

CPF LIFE provides lifelong monthly payouts ranging from $940-$1,000 for Basic Retirement Sum holders, $1,850-$2,000 for Full Retirement Sum, and $2,700-$2,900 for Enhanced Retirement Sum in 2025. The system functions as national longevity insurance that protects against outliving savings.

That's what I mean by converting wealth into certainty. You're taking a portion of assets and assigning them a fixed role, instead of leaving everything exposed to the same set of risks.

Why the Industry Resists This Shift

As for why the industry doesn't do this more systematically, a few forces tend to get in the way. First is how success is measured. Performance is visible and comparable. Certainty is quiet. If a client's income remains stable during a downturn, it doesn't show up as "outperformance." It just looks uneventful.

But uneventful is exactly what most retirees are trying to buy.

Second is incentive structure. Much of the industry is still built around assets under management. When assets are converted into income streams like annuities, they often move outside that framework. So the system naturally leans toward keeping assets invested rather than repositioning them for stability.

Third is discomfort with trade-offs. Advisers are trained to optimize, not to simplify. Saying, "this portion no longer needs to grow" can feel like leaving value on the table. But in reality, it's often removing a hidden liability.

Not every dollar needs to perform. Some dollars need to hold the line.

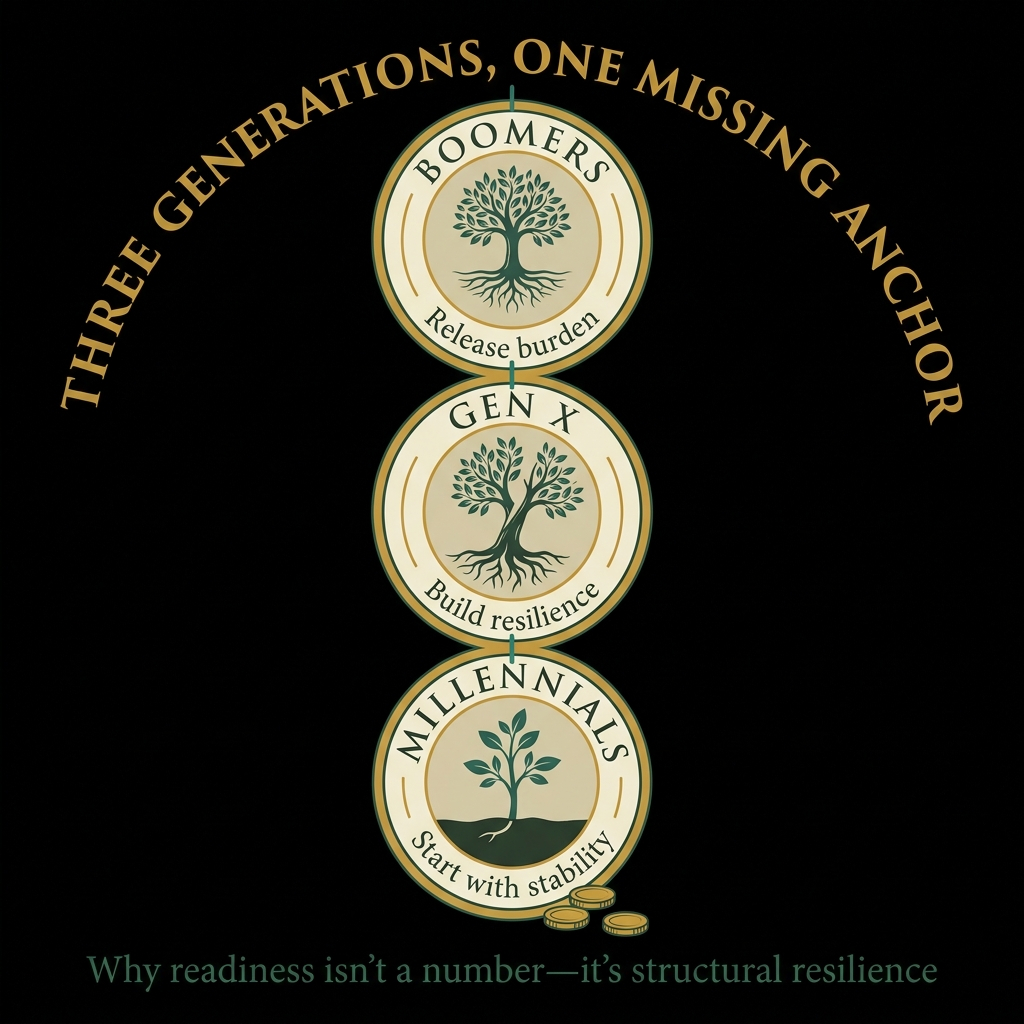

What Each Generation Needs to Hear

There's a pattern that only becomes visible after watching different generations approach the same problem from different starting points. The numbers change, the tools evolve, but the underlying blind spots tend to repeat in slightly different forms.

Each generation isn't missing information. They're often just holding onto the wrong definition of readiness.

For Boomers: Release Future Burden

The quiet risk isn't whether you've accumulated enough. Many have. The issue is how much of that wealth is still exposed to decisions you may not want to keep making.

This is the group that was taught to value control. Stay invested. Stay flexible. Keep options open. That worked during accumulation. But in retirement, too much control can turn into ongoing responsibility.

Converting a portion of assets into predictable income through structures like CPF LIFE or similar instruments isn't about giving up control. It's about releasing future burden. Especially in the later years, when managing complexity becomes less appealing.

Many Boomers don't need better returns. They need fewer moving parts. The real risk isn't running out of money. It's gradually losing the clarity and confidence to use it.

For Gen X: Build Resilience Over Optimization

The tension feels different for this group. Often caught between responsibilities. Aging parents, children still not fully independent, and their own retirement approaching faster than expected.

They tend to be financially aware, but structurally stretched. The industry often tells them to "catch up" or "invest more aggressively." But that advice sometimes misses the real issue. Their plans are often too tightly coupled to a single timeline.

Resilience matters more than optimization at this stage. Instead of asking, "Am I on track for retirement at 65?" a more useful question is, "If one part of my life shifts, does everything else start to strain?"

Building a buffer of liquidity, securing a baseline future income, and reducing dependencies between moving parts often matters more than squeezing out higher returns. Gen X doesn't need a perfect plan. They need one that doesn't break easily.

For Millennials: Start With Stability, Not Growth

The challenge is almost the mirror image. They have time, but they're facing uncertainty. Career paths are less linear. Housing decisions feel heavier. The cost of committing early can feel high.

So the instinct is to stay flexible, delay locking anything in, and focus on growth. That instinct isn't wrong. But it can quietly drift into a form of indefinite postponement.

Retirement readiness doesn't begin with investing. It begins with income stability and cash flow clarity. Before thinking about maximizing returns, there's a need to stabilize the base. Emergency liquidity. Insurance for major disruptions. A clear sense of essential versus discretionary spending.

Without that, investing becomes emotionally fragile. Every downturn feels personal because there isn't a stable foundation underneath.

Engineering Plans That Hold When Belief Fails

That moment is more common than most people expect. It usually doesn't arrive with a crisis. It comes quietly, often during a market drawdown, when the numbers still say "you're fine," but the client no longer feels fine.

Engineering for that moment means accepting one uncomfortable truth early. At some point, the client will doubt the plan. The design has to assume that loss of belief will happen, not try to prevent it.

So the question becomes: What continues to function without requiring belief?

Essential expenses need to be funded in a way that does not depend on markets, forecasts, or ongoing decisions. When income continues to arrive regardless of what's happening externally, the plan doesn't ask the client to stay calm in order to work. It just works.

This is where structures like CPF LIFE become more than a component. They become a behavioral safeguard. The client doesn't need to trust markets, or even trust themselves in that moment. The income shows up anyway.

Without that separation, the client is forced into a position where belief is required to maintain the plan. And belief is fragile under stress.

The Overlooked Reality of Permission to Spend

Most retirement plans are built around financial sufficiency. But what actually determines how a plan plays out is permission to spend.

I've sat with clients who clearly have enough. The numbers work. The buffers are there. Income is stable. But they still hesitate. They defer travel. They scale down experiences. They hold back, not out of necessity, but out of uncertainty.

And on the surface, it looks responsible. But over time, it becomes a different kind of risk. A life that was financially successful but gradually under-lived.

What I've come to realize is that readiness isn't just about having enough. It's about knowing, with enough clarity, that you're allowed to use it.

When essential income is clearly covered, often through something like CPF LIFE, and when the rest of the portfolio has defined roles, something shifts. Spending stops feeling like a risk decision and starts feeling like a choice.

Without that clarity, every dollar spent carries a question mark. "Will I need this later?" "Am I taking too much too early?" "What if something goes wrong?"

Even if those fears are statistically unlikely, they shape behavior in very real ways.

Why the Gap Keeps Widening

If a framework is sound, you'd expect outcomes to improve. But what's actually happening is that the environment people are trying to retire into has changed faster than the advice model has adapted.

The gap is widening not because people are ignoring advice, but because the advice is still optimizing for a world that's slowly disappearing.

The system shifted risk from institutions to individuals, but didn't fully redesign how plans should be built under that new reality. We're living in a more information-dense environment. Clients don't just review their portfolios quarterly. They see movements daily, sometimes hourly.

That constant exposure makes it harder to stay the course, even for disciplined people. So even if the underlying plan is reasonable, the experience of living through it has become more volatile.

There's also a structural mismatch in how success is defined. The industry still leans heavily on accumulation metrics. Net worth. Returns. Probability projections. But most people don't fail retirement because they didn't hit a number.

They struggle because their plans can't absorb real-life disruptions. Job loss in the late 50s. Supporting parents longer than expected. Healthcare costs that arrive unevenly. Children who need more time.

These aren't rare events. They're normal life paths. But plans are still often built as if life will follow a relatively smooth trajectory.

People are told they're "on track" based on a model. But their lived experience keeps deviating from that model. Over time, that creates a quiet distrust. Not just in the plan, but in the entire idea of readiness.

That's where the widening gap really comes from. It's not just a financial gap. It's a confidence gap.

What Actually Works

Designing for stability, decision reduction, and behavioral resilience often leads to recommendations that are less exciting, less optimizable, and sometimes less commercially attractive. It may involve allocating to things like CPF LIFE, holding more liquidity than feels efficient, or deliberately simplifying structures.

Those decisions don't always show up well in performance comparisons. They don't maximize returns in good years. And they require a shift in how both advisers and clients define "good outcomes."

But at an individual level, plans that are built for continuity rather than optimization tend to hold their shape much better over time.

The industry tends to frame readiness as a number or a rate of return. But in practice, readiness feels more like how much of your life is protected from things not going to plan.

For some, that means converting assets into dependable income. For others, it means reducing reliance on a single outcome. For younger clients, it means building a base that can absorb shocks.

Different expressions, same underlying idea. A plan isn't ready because it looks complete. It's ready because it can continue to function when conditions change and when the person living through it changes too.

In the end, the most successful plans I've seen aren't the ones that maximize outcomes. They're the ones that create enough clarity for the client to live without constantly checking if they're still okay.

Because at that point, the plan has done something more than just sustain wealth. It has restored a sense of ease in how life is lived.

These are conversations I’ve been having more often in recent years. Not about returns, but about how to make plans hold when life doesn’t go to plan.

No instruction. No urgency. Just an open door.

Warmest regards

Hanwei